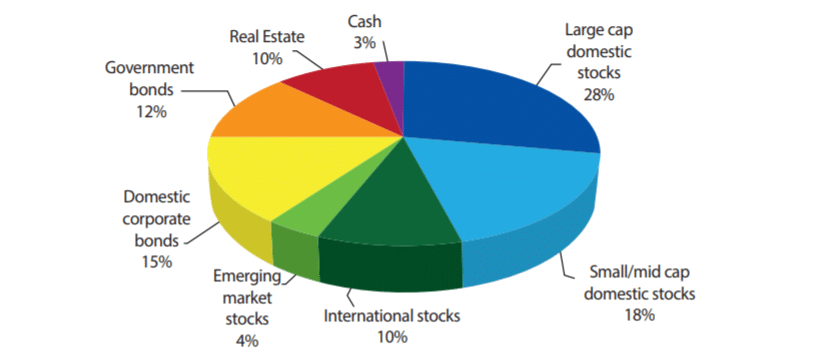

Sometimes I forget that many of you don’t understand some of the basics when it comes to investing. It is very easy to lose track when, not only have I been managing money for twenty years, but my Dad has a long history of investing as well. Did you talk about investing in stocks and bonds with your parents? Probably not. So let’s break this down to the absolute simplest terms possible. As I said, I often assume my readers understand certain concepts. If you don’t, the rest of the information may be hard to understand. When most people invest money, instead of buying a bunch of individual stocks, they put the money into mutual funds. Mutual funds consist of hundreds or thousands of holdings within one investment vehicle. When somebody says “You should have a diversified portfolio,” it simply means you need to spread the money around. Mutual funds are a great way to do this. I generally recommend against single stocks as they can be quite volatile and unpredictable. History shows a very predictable pattern of the total stock market, but individual stocks can do anything. And I don’t care if a company has been around for a long time. That does not mean it will make money. For example, GE has been around forever. It is down 65% over the past couple of years. Heinz is down 60%. Remember Texaco? It was one of the biggest companies in the country at the time. It went to zero. When you buy a mutual fund, the mutual fund has a ticker symbol. You need to know the ticker symbol to buy the mutual fund. Let’s say, you walk into Charles Schab or Fidelity, and you ask them to purchase $100,000 of SPY. What are you actually investing in? SPY is a fund that consists of the 500 largest companies in the U.S. all in one neat package. It means you would put: $5,800 into Apple $5,490 into Microsoft $4,170 into Amazon $4,070 into Google $2,260 into Facebook $1,480 into Berkshire Hathaway $1,320 into Tesla $1,290 into NVIDIA Corporation $1,290 into JP Morgan Chase $1,210 into Johnson and Johnson $1,100 into Visa $1,050 into United Healthcare $920 into Proctor and Gamble $910 into Home Depot This list goes on and on until it totals $100,000. You will own shares in 500 companies. The bigger the company, the bigger the allotment. Many of you have 401k funds through your company. Maybe you have been told that “You need a balanced and diversified portfolio.” You don’t want to put money only in large U.S. companies. Besides big American companies, there are other places to invest your money such as: Small-Sized Companies (there are called “Small Cap”) Medium-Sized Companies (Mid Cap) International Companies (Companies from first world nations) Emerging Market Companies (Companies from developing nations) You can also invest money in bonds. If you remember from past articles, a bond is simply a loan. For example, you loan Walmart $10,000 to help them build a store. They pay you 3% interest for ten years and then pay the loan back to you. Bonds often do well when stocks are doing poorly. The types of bonds are: U.S. Government Bonds (You are loaning money to the U.S. federal government) Municipal Bonds (Loans to municipalities) Corporate Bonds (Loans to companies) International Bonds (Loans to companies and governments overseas) So a “diversified and balanced portfolio of stocks and bonds” might look like: 30% Large Cap 10% Small Cap 10% Mid Cap 10% International 10% Emerging Markets 10% U.S. Government Bonds 10% Municipal Bonds 10% Corporate Bonds *This is an example portfolio. I am not giving you advice on how to invest your money. In addition, different asset classes move in different directions at different times. In 2007 Emerging Markets made 40% and Small Companies lost 2%. In 2008 U.S Treasury Bonds made 5% and Large Companies lost 37%. In 2013 Small Companies made 39% and Emerging Markets lost 3% In 2014 Large Companies made 14% and International lost 5%. Last year Small Cap was the best with a 20% gain and Bonds were the worst with a 6% gain. So you can see that it is important to spread your money around. Nobody knows in any given year which asset classes will thrive and which will do poorly. Don’t try to chase good returns. For example: In 2017 Emerging Markets made the most and in 2018 they lost the most. In 2018 Small-Cap was one of the worst and in 2019 it was one of the best. Even though everyone has opinions on what kinds of asset classes are going to do well, they have no idea what they are talking about. Be Blessed, Dave |

No comments:

Post a Comment