Family Update

Our dog is half Golder retriever and half miniature poodle. We never saw him swim before, so we decided it was time to try it out. We threw him in the pool, not knowing what to expect. He loved it!

We had a great Mother’s Day at the beach. She was able to hang out with our kids and a few cousins stopped by as well. We fished for Mangrove Snapper, cracked open coconuts lying on the beach, and played in the sand. We truly live in paradise.

I would prefer it if everyone else in this country never finds out. I think it might be too late.

I’ve had quite a number of you reach out concerned about the state of the country and the world. I can talk most of them off the cliff, but many still say:

“Ok Dave, I know investing worked in the past, but this time it’s different.”

Sir John Templeton was an extremely successful investor, banker, fund manager, and philanthropist. Having lived until ninety-six, he personally experienced nearly a hundred years of the ups and downs of the markets.

After all those years, he famously said:

“The four most dangerous words in investing are: this time it’s different.”

I’ll show you what I mean through a few colorful anecdotes.

Robert Pinochle

The year was 1930. Robert Pincohle had $10,000 invested in the stock market. (A lot of money in 1930.) Robert thought to himself, “We are in the middle of the worst economic downturn this country has ever seen.” He was right about that, but what he did next was a mistake. He thought, “This time is different. The markets are dangerous.” Robert took all of his money in cash and buried it in his backyard. Ten years later, in 1940, his $10,000, had he had kept it in the stock market, would have been worth $11,925.

John Canterbury

The year was 1940. John Canterbury had $10,000 invested in the stock market. He thought to himself, “We are in the middle of another World War. Countries are collapsing! The economic predictions are dire. Government debt is at an all-time high. This time is different!” John took the money in cash and stored it under the bed in his wife’s best Tupperware. Ten years later in 1950, his $10,000, had he kept it in the stock market, would have been worth $35,035. And his wife wouldn’t have had to re-buy all those containers!

Earl Pickett

The year was 1950. Earl Pickett had $10,000 invested in the stock market. He thought to himself, “The Communists have infiltrated our government. I’m pretty sure my neighbor Bob is a Commie. A Communist takeover spells disaster for our country, and the market. This time is different.” Earl took the money in cash and hid it in his collection of Elvis Presley nesting dolls. Ten years later in 1960, his $10,000, if he had kept it in the stock market, was worth $44,694.

Paul Kowalski

The year was 1960. Paul Kowalski had $10,000 invested in the stock market. He thought to himself, “The stock market has been going up for nearly 20 years. We are due for a crash. This time is different.” Paul took the money in cash and hid it in the stuffing of his Day-Glo orange beanbag chair. Guess what? Ten years later in 1970, his $10,000, had he kept it in the stock market, would have been worth $21,959.

David Malkin

The year was 1970. David Malkin had $10,000 invested in the stock market. He thought to himself, “This country is falling apart. Vietnam. Oil embargoes. Hippies. This time is different.” David took the money in cash and buried it in his backyard, putting his Pet Rock on top to guard it. Ten years later in 1980, his $10,000 would have been worth $22,555 … if he’d kept it in the stock market. Bummer, man.

Tom Chadwick

The year was 1980. Tom Chadwick had $10,000 invested in the stock market. He thought to himself, “The Cold War menace is looming. Nuclear tensions are at an all-time high. Russian paratroopers could descend from the skies at any time. This time is different.” Tom took the money in cash and buried it in his backyard. Ten years later in 1990, his $10,000, had he kept it in the stock market, was worth $36,813.

Wolfgang Applebottom

The year was 1990. Wolfgang Applebottom had $10,000 invested in the stock market. He thought to himself, “Saddam Hussein has us on the brink of war. Stocks are overvalued. We haven’t had a significant recession since the early 70s. This time is different. The markets are dangerous.” Wolfgang took the money in cash and stuffed it into his wife’s collection of Beanie Babies. Ten years later in 2000, his $10,000, had he kept it in the stock market, was worth $49,907. Worse, his wife’s McDonald’s International Beanie Bear would have been worth $10,000, except Wolfgang tore all the stuffing out to hide his cash.

Bobby Bickleberry

The year was 2000. Bobby Bickleberry had $10,000 invested in the stock market. He thought to himself, “The tech bubble is bursting. I’m hearing rumors of a long-term recession. This time is different. The markets are dangerous.” Bobby took the money in cash and stored it in a safety deposit box at the bank. Ten years later in 2010, his $10,000, had he had kept it in the stock market, would have been worth $11,500 (after two of the worst bear markets in U.S. economic history).

Derek Johansen

The year was 2010. Derek Johansen had $10,000 invested in the stock market. He thought to himself, “We just experienced a decade with two historically awful recessions. I am spooked. No more investing for me!” Derek took the money in cash and locked it in a fire-proof safe, which he kept in his closet. Nine years later in 2019, his $10,000, had he had kept it in the stock market, would have been worth $32,016.

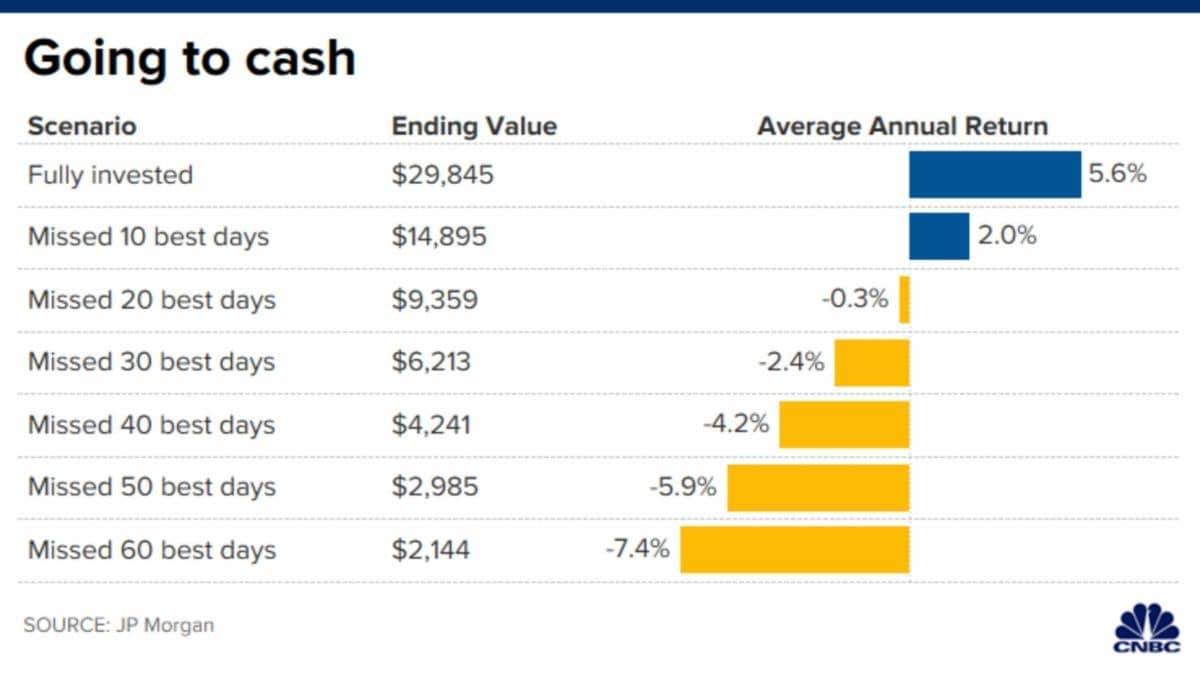

Maybe this time isn’t different. Maybe it’s time to embrace a financial vehicle that has an almost uninterrupted string of success for decades. Markets temporarily go down and permanently go up.

Be Blessed,

Dave